From soaring electricity bills to collapsing insurance markets, the costs of extreme weather are no longer abstract, they're arriving monthly in American mailboxes. But the policy cure may be as dangerous as the disease.

By the Energy & Environment Desk, Hemera Networks

WHAT'S NEWS

Extreme weather has cost the global economy more than $2 trillion since 2014, with 2022–23 damages alone reaching $451 billion, a 19% acceleration over the prior eight years.

US electricity prices are up 38% since 2020, rising at twice the rate of overall inflation; the average household bill hit $178/month in 2025 as grid capacity tightens against AI-driven demand.

Private insurers are withdrawing from high-risk states en masse, with California's insurer of last resort tripling its policyholder base since 2018 and requiring a $1 billion emergency bailout following the 2025 LA wildfires.

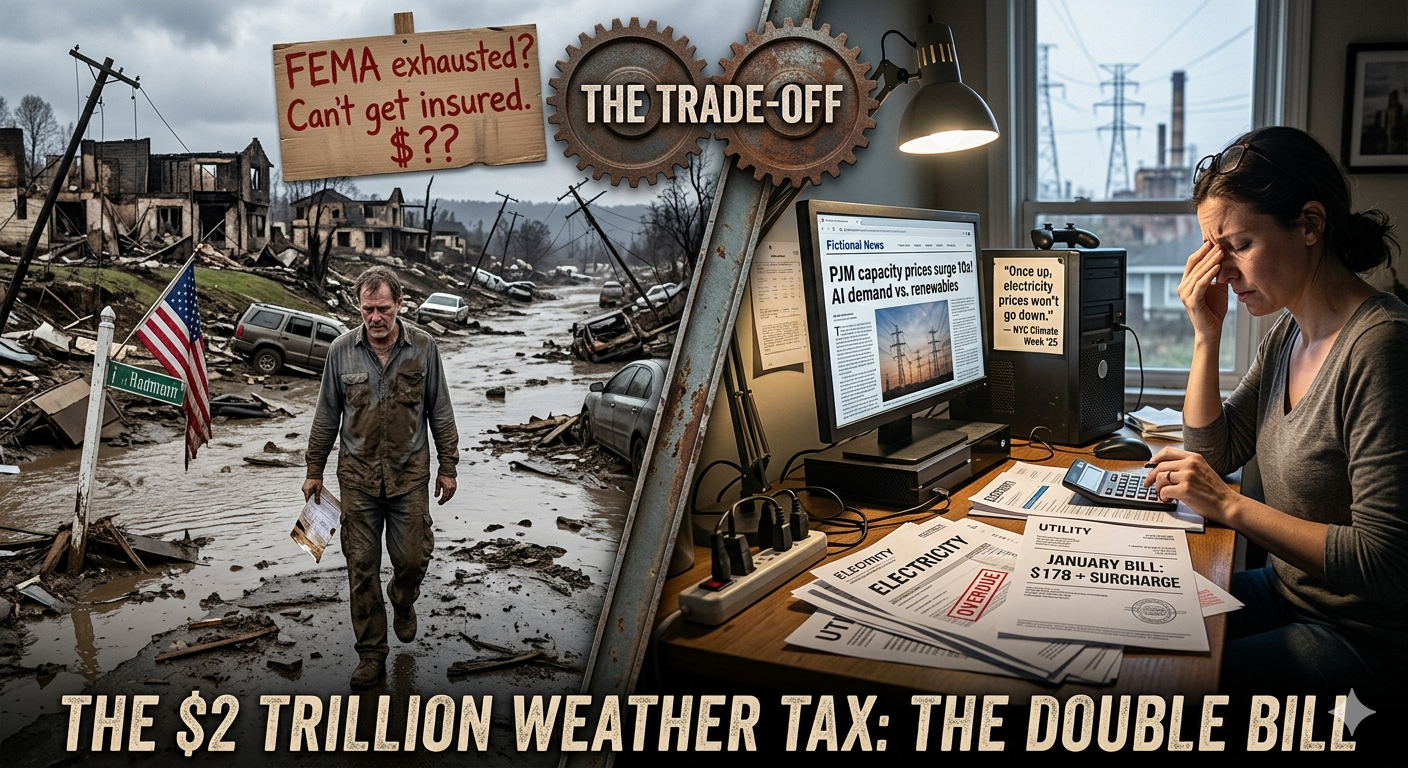

The bill is in. Extreme weather driven by a destabilising climate has cost the global economy more than $2 trillion since 2014, touching nearly 1.6 billion people across nearly 4,000 recorded events, from Bangladesh's catastrophic 2024 floods to California's January 2025 wildfires, which alone torched an estimated $250 billion in economic value from a single metropolitan region. For decades, the cost of climate disruption was treated as a future accounting problem. That pretence is over. The damages are present, compounding, and increasingly uninsurable.

Yet here is the central paradox no politician wants to answer plainly: the remedies being deployed to arrest climate change are themselves generating a separate and immediate inflation, an electricity price surge, a grid reliability crisis, and an energy policy tangle that is quietly strangling industrial output and household budgets simultaneously. America faces not one cost spiral but two, and Washington has thus far failed to honestly account for either.

Once they're up, we can't get electricity prices back down. Period.

- energy policy panelist, NYC Climate Week 2025

THE STORM DAMAGE LEDGER

The numbers from the damage side are not in dispute. In the US alone, losses from billion-dollar weather disasters have averaged $140 billion per year over the past decade, according to NOAA, with 2024 recording 24 confirmed events of that magnitude. In Europe, annual economic losses from climate-related extremes rose from an average of €8.6 billion in the 1980s to €44.9 billion per year between 2020 and 2024, a fivefold increase in a single generation. The Bank for International Settlements confirmed in early 2025 that droughts and wildfires temporarily raise food and energy prices, with lasting GDP depressions, particularly in agriculture-dependent and hydro-reliant economies like Brazil, where reservoir shortfalls in 2024 forced emergency electricity surcharges.

This is not merely an environmental story. It is a structural macroeconomic story. Droughts cut hydroelectric output. Floods destroy supply chains. Wildfires obliterate property wealth and the tax bases that fund rebuilding. Hurricane Helene, which made landfall in late 2024 as a Category 4 storm, caused unprecedented inland dam failures as far inland as North Carolina, communities with no historical exposure to tropical systems. Eight days into fiscal year 2025, FEMA had already exhausted nearly half its annual disaster relief budget, with the rest of hurricane season still ahead.

THE INSURANCE MARKET IMPLOSION

The canary in the coal mine, so to speak, is the American property insurance market, and the canary is dead. Homeowners' average insurance premiums jumped 33% in nominal terms between 2020 and 2023, a 13% real increase even after stripping out general inflation, according to research published by the National Bureau of Economic Research. In the five costliest states, Nebraska, Louisiana, Florida, Oklahoma, and Kansas, homeowners now pay upwards of $4,400 annually, more than double the national average of $2,400. In Florida, the worst-hit market, average premiums reached $15,000 for some properties.

The private market's response has been withdrawal, not adaptation. In 2023, insurers lost money on homeowners' coverage in 18 states, up from 8 in 2013. Major national carriers stopped writing new policies in California. Four separate insurers exited Iowa entirely due to severe convective storm losses. California's FAIR Plan, the state's insurer of last resort, tripled its policyholder base to over 610,000 by mid-2025, nearly all of them homeowners with nowhere else to turn. When the 2025 Los Angeles wildfires struck, that plan required a $1 billion bailout, costs of which were distributed across all California policyholders. In effect, taxpayers and stable-risk homeowners are now quietly subsidising the consequences of decades of building in fire-prone terrain.

The cascading consequences extend further than insurance premiums. As property values fall in climate-exposed areas, municipal tax bases shrink, cutting funding for the emergency services needed to respond to the very disasters causing the retreat. It is a vulnerability double-bind of the most punishing kind.

THE POLICY INFLATION: THE OTHER BILL

Now enter the political response, and with it, a second wave of economic pressure that complicates the picture for anyone inclined to treat climate mandates as costless virtue. US electricity prices rose 38% between 2020 and 2025, now increasing at roughly twice the rate of overall consumer inflation. A poll conducted in late December 2025 found that 68% of voters ranked energy affordability as their top policy priority, against only 18% who prioritised clean energy usage. This is not a fringe position. It tracks with a material reality: the average American household electricity bill hit $178 per month in 2025, up 13% from 2022 alone.

What is driving this? The honest answer implicates multiple actors. Natural gas, still supplying 42% of US grid power, has seen its price rise 45% year-on-year as of October 2025. Carbon cap-and-trade programmes in the Northeast have pushed compliance costs onto ratepayers; the four most recent Regional Greenhouse Gas Initiative auctions collected $1.4 billion, five times their 2019 yield, with costs passed directly to consumers. Renewable portfolio standards, requiring utilities to purchase a mandated share of higher-cost green energy, have added further upward pressure in states that also decommissioned dispatchable baseload ahead of schedule. New Jersey shut the Oyster Creek nuclear plant in 2018; today it faces an AI-driven load surge with no firm baseload margin to absorb it.

California offers the starkest case study. Over 70% of US transmission infrastructure is past the midpoint of its 50-year design life. Annual expenditure on transmission has hit record highs, yet 90% of that spending replaces aging equipment, not new capacity. Meanwhile, wildfires have forced utilities to spend massively on risk mitigation, with grid hardening identified as the single largest driver of California's rate increases over the past five years. The cost of climate damage and the cost of the energy transition are now indistinguishable on the electricity bill, and the consumer pays both.

AI POURS ACCELERANT ON THE FIRE

If policymakers thought the grid stress was already severe, the artificial intelligence boom has redrawn the demand curve in ways that expose every structural weakness simultaneously. Total US data centre electricity use tripled over the past decade and is projected to double or triple again by 2028. In Virginia, host to the world's densest concentration of data centres, residential power costs are projected to rise 26% this decade and 41% in the next. PJM Interconnection, the largest US grid operator, projects approximately 32 gigawatts of new peak load by 2030, with roughly 30 of those gigawatts attributable to data centres alone.

The capacity market tells the real story. PJM's capacity market-clearing price jumped almost tenfold from 2023 to 2024, from $29 per megawatt-day to $270. By July 2025, it had risen again to $329. These prices reflect a grid that is being asked to do more with less dispatchable supply. Intermittent wind and solar, by physical definition, cannot guarantee availability when demand peaks, during heat waves, winter cold snaps, or continuous AI compute loads that run 24 hours a day, 365 days a year. The storage batteries that would theoretically fill these gaps remain prohibitively expensive at any scale approaching grid adequacy, a fact that data centre operators apparently understand better than many energy ministers: an increasing share of hyperscale operators are quietly seeking contracts with nuclear, natural gas, or even coal plants for firm, continuous power.

HISTORICAL ECHOES: FAILED PROMISES AND FRESH PRETENCES

None of this should be entirely surprising to anyone with a memory longer than a single policy cycle. The 1970s oil shocks generated exactly this combination: a real physical disruption followed by a political scramble that produced expensive mandates, misallocated subsidies, and false promises of energy independence. The Carter administration's Synthetic Fuels Corporation, capitalised at $88 billion in today's terms, produced almost nothing commercially viable before being dismantled in 1986. The ethanol mandates of the 2000s diverted corn from food markets, raised food prices globally, and delivered emissions reductions that serious analysis found were largely negligible compared to conventional gasoline. The lesson each time was the same: mandating outcomes without respecting physical and economic constraints does not accelerate the transition. It discredits it.

The current moment risks repeating this error at greater scale. EV mandates that assume a charging infrastructure that does not yet exist at adequate density or grid capacity. Net-zero pledges from corporations that simultaneously lobby against the transmission permitting reform needed to build the renewable capacity their pledges require. Federal subsidies for offshore wind projects that were cancelled when real-world costs proved double the contracted estimates. The pattern of overpromising and underdelivering is not incidental, it is structural, emerging whenever political timelines are imposed on physical systems that obey different clocks.

THE BOTTOM LINE

The climate cost is real and growing. The $2 trillion in extreme weather damages over the past decade is a floor, not a ceiling, as the BIS and multiple independent research bodies have noted. The property insurance crisis is a leading indicator of what happens when financial markets are forced to price physical risk that governments have long subsidised into invisibility. These costs are not optional; they are arriving regardless of policy preference.

But the policy response must be held to the same rigorous accounting. Electricity bills rising at twice the rate of inflation are not an abstraction. Thirty-four percent of American households cutting back on food or medicine to pay energy bills is not an abstraction. A grid that cannot reliably serve existing industrial demand while being simultaneously asked to electrify transport, heat homes, and power AI at continental scale is not a problem that slogans resolve. The nation needs energy that is secure, affordable, and progressively cleaner, in that order, because without the first two, the third becomes politically impossible. Any honest conversation about climate economics must begin there.

KEY FIGURES

$140B/yr - avg US billion-dollar disaster losses, past decade (NOAA)

$329/MW-day - PJM capacity market clearing price, July 2025, up from $29 two years prior

$250B - estimated economic loss from 2025 LA wildfires alone

34% - US households cutting food/medicine to pay energy bills

32 GW - projected new US peak demand by 2030, ~30 GW from data centres

THE TRADE-OFF

Who pays the double bill?

American households are caught in a squeeze with two jaws. The first is the direct cost of climate damage: insurance premiums up 33% in three years, FEMA disaster relief perpetually insolvent, and property values quietly eroding in flood and fire corridors.

The second jaw is the cost of the policy response. Carbon compliance programmes, renewable portfolio mandates, and early baseload retirements have added measurable cents per kilowatt-hour to bills in nine states. In Virginia, ratepayers face a projected 41% hike in power and transmission costs over the next decade, driven simultaneously by grid hardening costs and AI data centre load growth.

Neither jaw can be ignored. But policymakers have been selective in their accounting, citing climate damage as justification for mandates while deflecting scrutiny of those mandates' own cost impact. The trade-off the public deserves to see, plainly stated: the transition away from fossil fuels is necessary, but it is not free, and the bill is already being distributed - disproportionately to lower-income households least able to absorb it.

Hemera Networks | Reporting draws on data from NOAA, Bank for International Settlements, International Chamber of Commerce/Oxera, NBER, Yale Law Journal, Lawrence Berkeley National Laboratory, PJM Interconnection, EIA, and the US Joint Economic Committee. This article represents independent editorial analysis and is not investment advice.