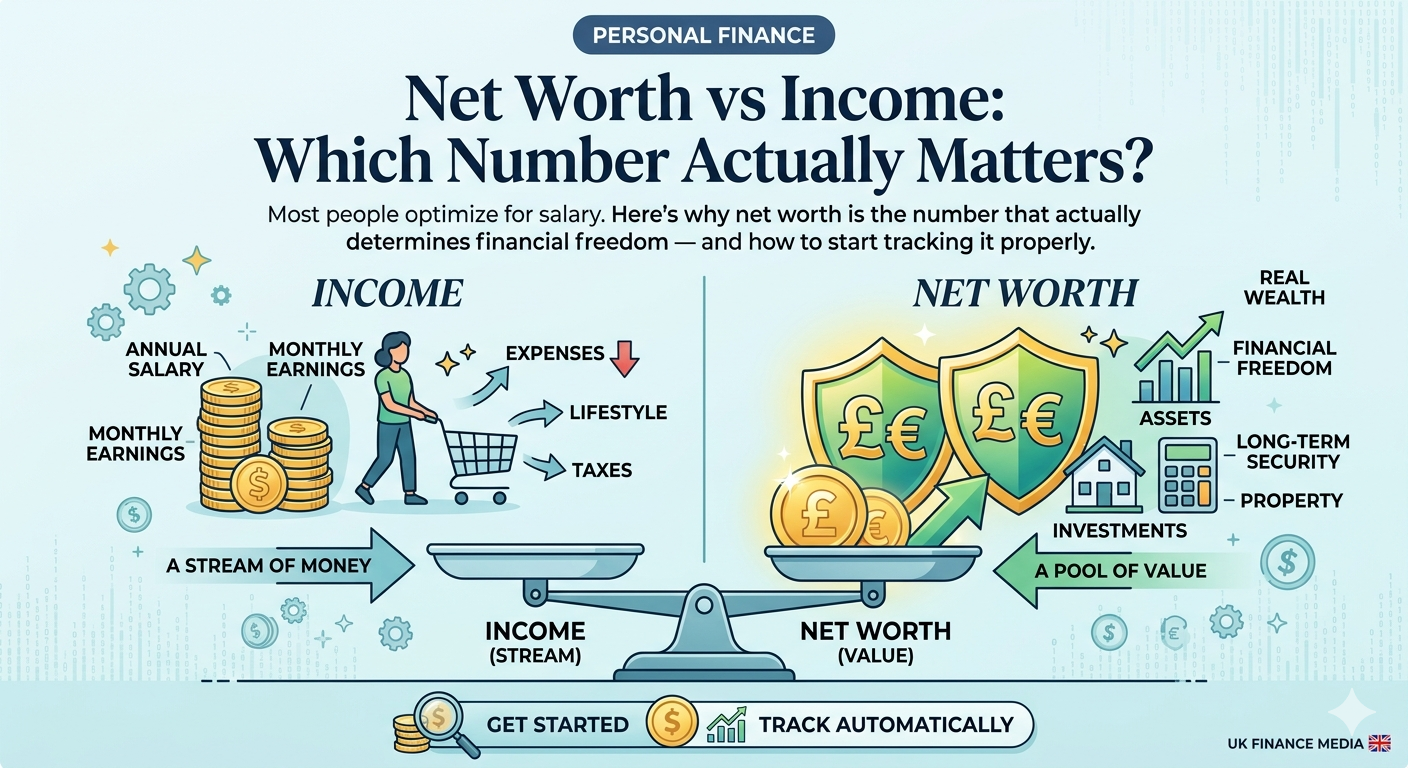

The most important number in your financial life isn't your salary. It's your net worth.

Your salary tells you what you earn. Your net worth tells you what you've built. And for most people in the UK, it's a number they've never actually calculated.

This guide will show you exactly how to do it - what to include, what people miss, and how to track it over time without building a spreadsheet.

What Is Net Worth?

Net worth is simple: everything you own, minus everything you owe.

Assets − Liabilities = Net Worth

If your assets total £150,000 and your debts total £80,000, your net worth is £70,000. If your debts exceed your assets, your net worth is negative - which is completely normal early in adult life, especially if you have a student loan or mortgage.

The goal isn't to have a high net worth today. It's to watch it grow consistently over time.

What Counts as an Asset in the UK?

This is where most people undercount. Your assets include:

Cash and savings

Current accounts

Savings accounts

Cash ISAs

Emergency fund

Investments

Stocks and Shares ISA

General investment account (GIA)

Bonds, ETFs, individual shares

Pensions - the most overlooked asset

Workplace pension (check your most recent statement for the current value)

Self-Invested Personal Pension (SIPP)

State Pension (you can get a forecast at gov.uk/check-state-pension)

Property

Your home (use Zoopla or Rightmove estimates for a reasonable market value)

Buy-to-let properties

Any other property

Other

Cryptocurrency

Business equity (if self-employed or a business owner)

Vehicles (at current market value, not what you paid)

Valuable items (art, watches, collectibles - only if you'd actually sell them)

What Counts as a Liability?

Secured debt

Mortgage outstanding balance (not the property value - the remaining debt)

Unsecured debt

Personal loans

Credit card balances

Car finance

Buy-now-pay-later balances

Student loans

Plan 1, Plan 2, or Plan 5 - include the balance, though for most people this functions more like a graduate tax than a traditional debt

The Calculation

Add up all your assets. Add up all your liabilities. Subtract.

Done once, this gives you a snapshot. Done monthly, it tells a story.

Why Most People Don't Do This

The honest answer is that it's annoying. Logging into eight different apps - your current account, your ISA platform, your pension provider, your mortgage portal - to collect the numbers, then manually adding them up in a spreadsheet that you'll probably lose, is not something most people do consistently.

Which is why the tracking almost always stops after the first month.

How to Track It Automatically

FinPath Navigator is a UK personal finance app built specifically for this. You connect your accounts - cash, ISAs, SIPPs, pensions, property, crypto - and it calculates your net worth automatically, tracks it over time, and shows you the trajectory.

It's free to start, and unlike most finance apps, it actually understands UK financial products. It knows what a SIPP is. It knows what a Stocks and Shares ISA is. It handles GBP natively.

You can try it free on Android or Web with no card required.

How Often Should You Check Your Net Worth?

Monthly is the right cadence for most people. More frequently than that and you'll obsess over short-term market movements. Less frequently and you lose the sense of momentum.

Set a recurring reminder on the first of each month. Open your tracker. Update any values that have changed. Note the number. Move on.

Over 12 months, the chart becomes motivating in a way that a one-time calculation never can.

What's a Good Net Worth for Your Age?

There's no universal answer, but a rough UK benchmark used by financial planners is to aim for 1x your annual salary saved by 35, 3x by 45, and 6x by 55. These are guidelines, not rules - someone who started earning late, or who owns property, or who has a defined benefit pension, will look very different.

The only number that actually matters is whether yours is going up.

Start Today

Calculate your net worth right now, even roughly. Open a notes app. List your assets with estimated values. List your debts with outstanding balances. Subtract.

Then set up something to track it monthly so that number doesn't stay static.

FinPath Navigator is a UK personal finance app by Raina Corporation Limited. Free to download on Android.