WHAT'S NEWS

In April 2025, the United States imposed a baseline 10% tariff on all imports, with elevated country-specific rates Vietnam at 46%, and a 25% targeted levy on $300 billion of Chinese goods covering semiconductors, electronics, EV batteries, and rare earth minerals. China responded in kind, escalating retaliatory duties on over $200 billion of U.S. goods, eventually reaching 125% by mid-April.

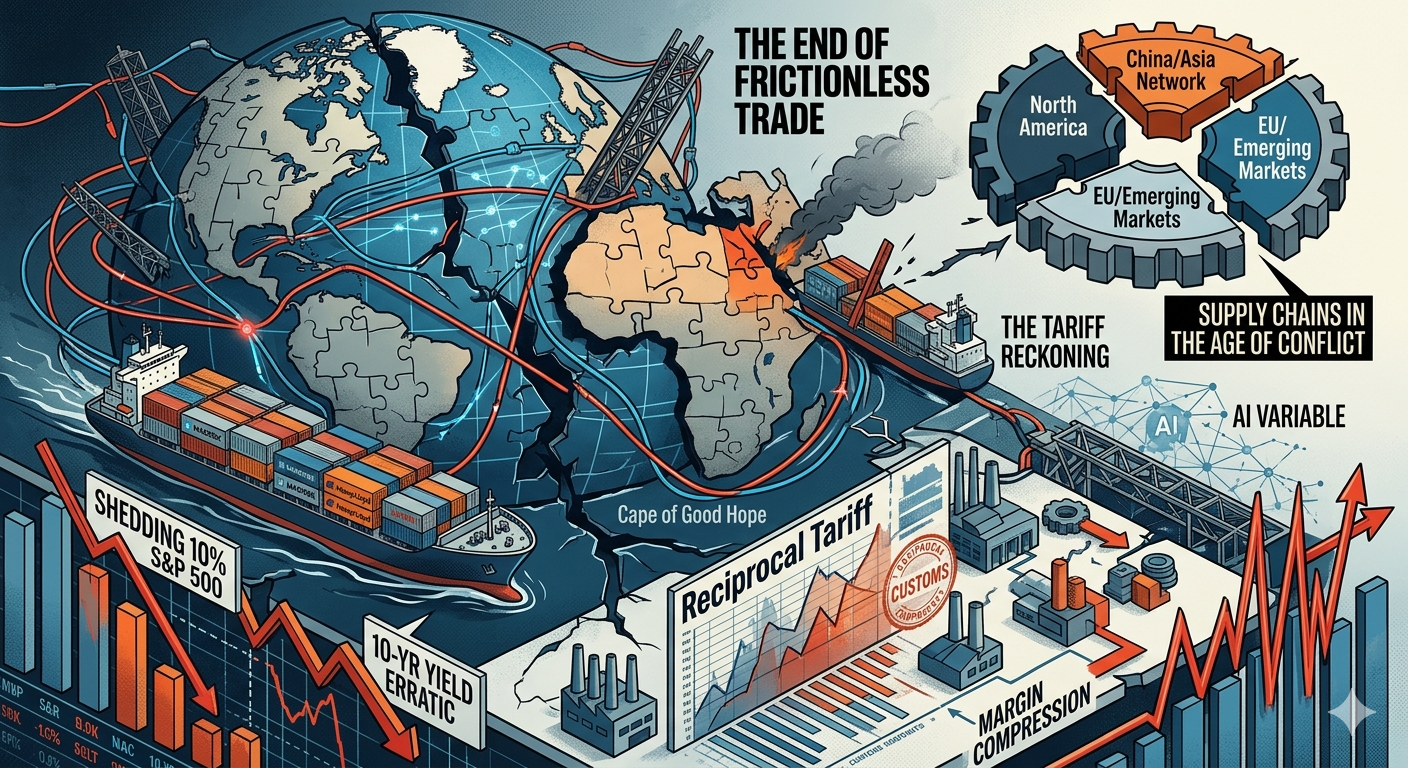

By May 2025, tonnage through the Suez Canal sat 70% below 2023 levels. Simultaneously, the Strait of Hormuz through which 11% of global trade and a third of seaborne oil transit, faced renewed disruption risks, and freight rate volatility was described by UNCTAD as "the new normal."

A McKinsey survey of 100 global supply chain leaders found 82% reported their operations were materially affected by new tariffs, with 20 to 40% of their supply chain activity impacted, and yet fewer than one in five planned to pass more than 80% of costs to customers.

The News Peg: When April Became a Turning Point

On April 2, 2025, a date that will likely appear in economics textbooks, the Trump administration unveiled what it called a "reciprocal tariff" framework that amounted to the most sweeping unilateral reshaping of global trade architecture since the Smoot-Hawley Act of 1930. The market reaction was swift: the S&P 500 shed roughly 10% in the days that followed before a 90-day pause was announced for most countries except China. The DJIA saw intraday swings not witnessed since the pandemic shock of March 2020. Bond markets told a more sobering story, the 10-year Treasury yield, which had been grinding toward 4.5%, jumped erratically as investors struggled to price the inflationary implications of a regime change in global trade policy.

What made this moment different from prior tariff rounds was not its scale alone, it was the simultaneity. UNCTAD noted that policy uncertainty had soared to record levels, driven by weakened multilateral rules, competition for raw materials, and the sheer speed of policy reversals a marked departure from the decades of relative stability that defined the post-WTO era.

The Thirty-Year Bargain and How It Broke

To understand where we are, one must understand what was built.

Between roughly 1990 and 2019, the world operated on an elegant and extraordinarily profitable theory: let each nation produce what it does best and trade the rest. The result was a global factory floor stitched together by container shipping, fibre-optic communications, and the WTO's rules-based framework. China became the workshop of the world. Germany became the precision-engineering hub. The United States became the innovation and consumption engine. Logistics optimised ruthlessly for cost and speed over redundancy and resilience. Inventories shrank. Lead times tightened. "Just-in-time" was not just a manufacturing philosophy, it was an ideology.

The first serious stress test came with COVID-19 in 2020, which revealed that a global supply chain optimised to a 3% margin of error had no tolerance for a 30% demand shock. The Russia-Ukraine war, Brexit, and intensifying U.S.-China trade tensions prompted observers to characterise the current era as a "new Cold War," with disruptions now stemming simultaneously from supply-side and demand-side shocks.

But the pandemic, for all its disruption, was ultimately a demand shock followed by a supply scramble. What has emerged since 2022 is structurally different: a deliberate political decision by the world's largest economies to trade efficiency for security. The vocabulary shifted, from "globalisation" to "friendshoring," from "offshoring" to "onshoring," from "supply chain optimisation" to "supply chain resilience." The words tell the story.

The Red Sea: When Geography Became Weaponised

On paper, the Bab al-Mandab Strait is a 29-kilometre chokepoint between Yemen and Djibouti. In practice, it is the jugular vein of Eurasian trade. Since October 2023, more than 200 Houthi attacks on vessels passing through the Suez Canal corridor have reshaped global maritime operations. The Suez Canal handles roughly 30% of global container traffic, and the immediate operational response was stark: Maersk, Hapag-Lloyd, MSC, and CMA CGM all diverted vessels around the Cape of Good Hope.

That rerouted journey adds approximately 7,000 to 11,000 nautical miles and extends transit times by 10 to 15 days. Fuel costs alone increase by roughly $300,000 per one-way trip approaching $1 million for a round trip on a large vessel between Asia and Europe. Multiply those numbers across the global fleet running this diversion for 18 months, and you begin to grasp why JPMorgan Research estimated the disruptions contributed an additional 0.7 percentage points to global core goods inflation in the first half of 2024.

Yet here is where the skeptical optimist pauses. By late 2025, even with most Asia-Europe services still routing around the Cape, container rates remained well below 2024 peaks, suggesting that fleet growth and overcapacity were now outweighing the impact of longer transit times. The market adapted. It always does. The question is what that adaptation cost in permanently rearranged trade flows, insurance premiums, and corporate capital allocation decisions made on the assumption that nothing is reliably safe anymore.

The Tariff Architecture: More Complex Than the Headlines Suggest

The popular narrative of tariffs runs like this: Trump imposes duties, China retaliates, trade collapses, inflation surges. The actual data is considerably more textured.

Between 2017 and 2022, China's share of U.S. imports fell from 22% to 16%, back to levels last seen in 2007. Yet total U.S. imports rose to nearly 40% above pre-COVID levels in 2022, implying that importers were not retreating from trade but simply redirecting it. The mechanism is revealing: in strategic industries, the countries replacing China as U.S. suppliers tend to be deeply integrated in China's own supply chains, meaning that to displace China on the export side, those countries first had to embrace China's production networks. Vietnam's 46% tariff rate in 2025 was partly a response to this dynamic a recognition that "Made in Vietnam" often meant "assembled in Vietnam from Chinese components."

After tariffs hit Chinese electronics, HP expanded sourcing to Taiwan and Thailand, reducing costs by 8%. Apple has accelerated plans to shift 15 to 20% of its production to India and Vietnam by 2026, having already invested more than $1 billion in Indian manufacturing facilities since 2023 though the transition has created a 10% increase in lead times for some products due to supply chain bottlenecks in Vietnam.

This is the iron law of supply chain restructuring: every move you make to reduce one risk creates at least one new risk. Cost, speed, or resilience in the current environment, you can reliably optimise for two.

The Corporate Playbook: Tactical Agility Over Strategic Transformation

McKinsey's 2025 supply chain survey found that tariffs had dominated supply chain leaders' attention, leading them to focus on tactical responses inventory shifts, supplier negotiations, nearshoring rather than long-term transformation. The initial impact appeared to be an acceleration of pre-existing resilience strategies rather than a fundamental redirection.

On the nearshoring front, GE announced a $3 billion investment to relocate refrigerator, gas range, and water heater production out of China and Mexico to the southeastern United States, while Samsung and LG made similar moves, shifting select home appliance production to South Carolina and Tennessee. GSK and Eli Lilly announced multibillion-dollar investments to build new U.S. pharmaceutical manufacturing plants.

A 2025 Deloitte study predicted that 40% of U.S. companies would relocate at least part of their supply chains to North America by 2026. That is a striking headline. The subtext is equally important: nearshoring requires substantial capital, and infrastructure gaps particularly in Mexico mean that the announced investment and the operational reality can diverge by years.

Across industries surveyed by McKinsey, the weighted average tariff pass-through rate to customers was only 45%, suggesting most companies planned to absorb or mitigate tariff effects elsewhere — a margin compression story that equity analysts pricing consumer staples and industrial names should note carefully.

The GVC Paradox: Still Alive, Just Reorganising

Here is the counterintuitive finding that most commentary misses. Despite years of disruption pandemic, geopolitical friction, financial shocks, climate challenges global value chains still account for 46.3% of global trade, not far off their 2022 peak of 48%. Rather than unravelling, GVCs are adapting by becoming more digital and more regional.

The world is not deglobalising so much as it is regionalising. Three rough blocs are consolidating: a Western-aligned network centred on the U.S., Canada, Mexico, and select EU partners; an Asian network that remains China-anchored despite political noise to the contrary; and an emerging Global South set of bilateral deals that defies easy categorisation. The OECD's 2025 Supply Chain Resilience Review concluded that the solution lies not in retrenchment but in re-architecting global networks to be more diversified, digitally enabled, and institutionally aligned with scale and agility no longer mutually exclusive.

For investors, this matters enormously. The companies that will dominate the next decade of industrial logistics are not necessarily the ones with the lowest-cost supply chains today they are the ones with the most optionality baked into their network architecture. Optionality has a price. It shows up in higher working capital requirements, redundant supplier relationships, and slightly lower short-term margins. Investors who penalise these companies for margin compression without understanding the strategic logic are, in effect, pricing out resilience.

The AI Variable: The One Force That Changes the Calculus

There is one development powerful enough to partially offset the cost headwinds of deglobalisation: artificial intelligence applied to supply chain management. AI has become one of the most transformative forces in global supply chains, enabling companies to move from reactive to proactive management. Starbucks, for instance, is deploying an AI-driven inventory counting system across North America that uses tablets to scan shelves in real time, instantly flagging low inventory. That is a modest example. The more consequential applications are in demand forecasting, multi-tier supplier risk modelling, and dynamic route optimisation precisely the capabilities that a fragmented, multi-sourced, regionally dispersed supply chain demands.

McKinsey's survey noted a slowdown in advanced digitisation investment as companies focused on tariff-related firefighting a troubling finding, since the leaders who resume their digital investment agendas soonest will be best equipped for the next wave of disruption. The lesson of 2020-2025 is that disruption does not pause while you restructure. The competitive advantage in supply chains will increasingly belong to firms that can absorb novel shocks in real time rather than those who planned perfectly for the last one.

What It Means: A Framework for Investors and Operators

The transition underway is not simply a political story or a logistics story. It is a fundamental repricing of risk in the global economy.

For equity investors, the implications cascade. Consumer discretionary names exposed to long single-sourced Asian supply chains carry risk that their P/E multiples may not yet fully reflect particularly if tariff regimes prove stickier than markets currently price. Industrial firms with flexible manufacturing footprints and digital inventory systems warrant a closer look at a premium. Shipping and logistics operators face a structurally bifurcated outlook: overcapacity suppressing freight rates on main lanes while geopolitical rerouting inflates costs on secondary routes a divergence that makes index-level exposure a blunt instrument.

For operators, the mandate is clear even if the execution is hard: build optionality now, before the next shock arrives and the options become expensive. Businesses must architect globally distributed, digitally empowered supply ecosystems that embed flexibility and optionality by design moving beyond the outdated notion that scale and agility are mutually exclusive. This means rethinking single-source dependencies, investing in real-time visibility platforms, and accepting that the cost structure of the next decade will not look like the last one.

The era of frictionless globalisation cheap, fast, efficient, fragile is over. What replaces it will be slower and more expensive in places, but almost certainly more durable. That is not cause for despair. It is, for the disciplined investor and the operationally agile firm, cause for careful attention.

Corrections & Amplifications

This article draws on data from UNCTAD's 2025 Maritime Trade Report, McKinsey's 2025 Supply Chain Risk Survey (n=100 companies), the WTO's Global Value Chain Development Report 2025, the Reshoring Initiative's 2024 Annual Report with Q1 2025 update, Deloitte's 2025 supply chain relocation survey, and JPMorgan Research estimates. Tariff figures reflect rates as reported by mid-April 2025 and are subject to ongoing negotiation and revision. Any reader who identifies a factual error is encouraged to contact the author directly for prompt correction and attribution.