What's News

Artemis II splashed down on April 10 after completing humanity's first crewed lunar flyby since Apollo 17 in 1972, setting a distance record of 248,656 miles from Earth and handing the Trump administration a rare political triumph framed explicitly as a counterweight to Chinese ambitions in cislunar space.

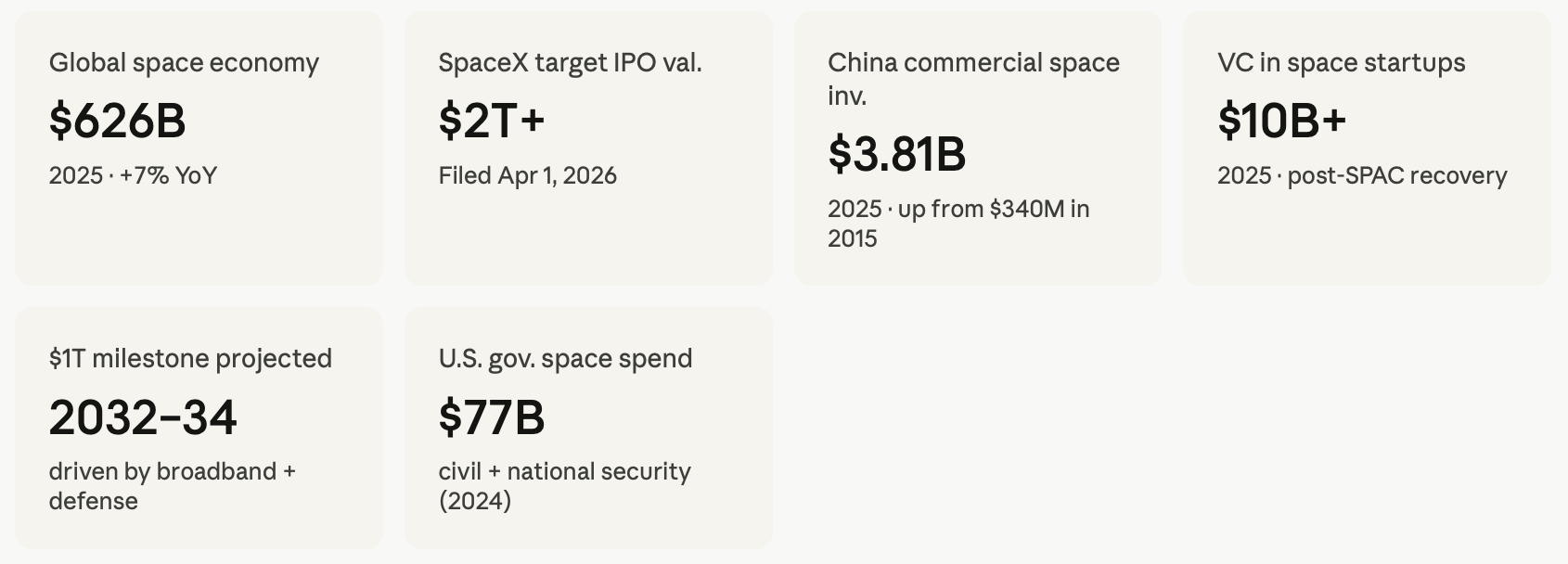

SpaceX confidentially filed for an IPO with the SEC on April 1, targeting a valuation above $2 trillion, which, if achieved, would make it the largest public offering in history and crystallize a profound structural shift in the space economy: the United States is running its great-power competition through private balance sheets, not government budgets alone.

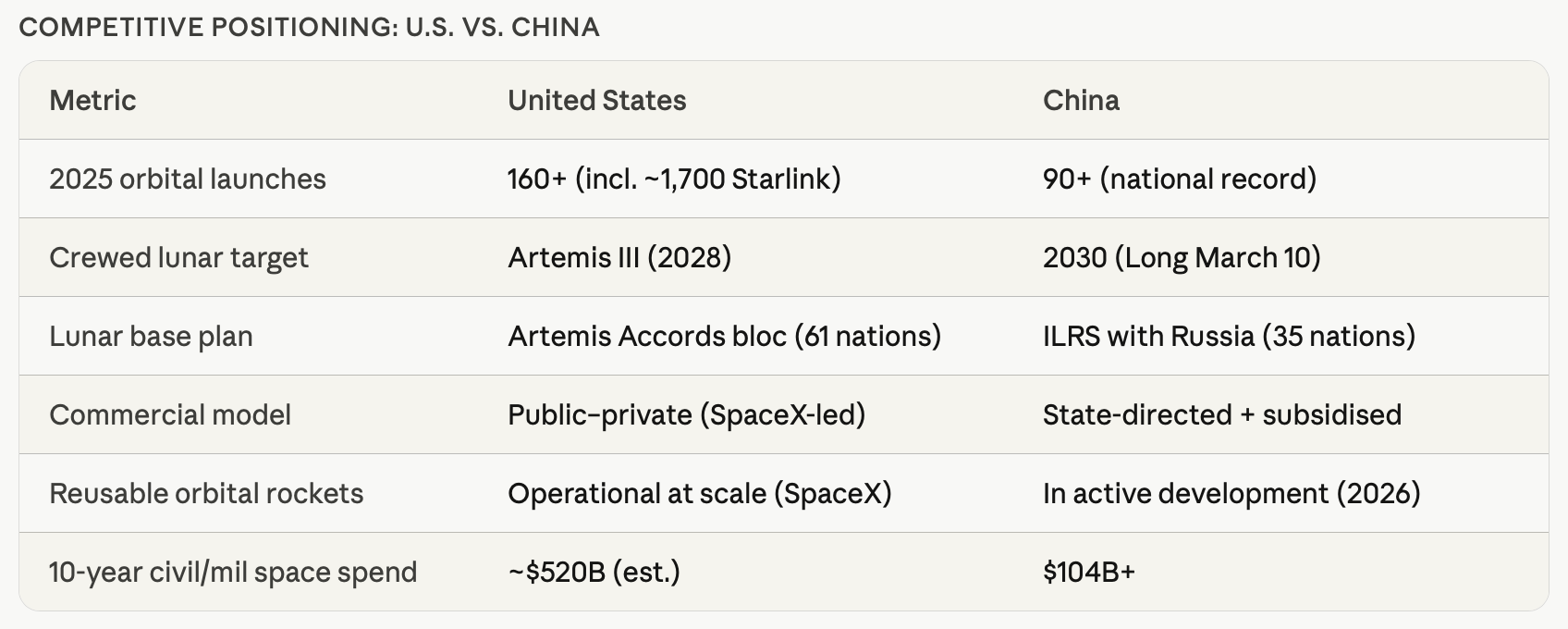

China conducted more than 90 orbital launches in 2025, a national record, while quietly completing key development milestones for its Long March 10 crewed rocket and Lanyue lunar lander, the hardware required to put taikonauts on the Moon's south pole by 2030 in a direct race against NASA's Artemis III, currently targeting 2028.

There is a genre of political theater in which the rocket is the message. When President Trump addressed the Artemis II crew, mission commander Reid Wiseman, pilot Victor Glover, and mission specialists Christina Koch and Jeremy Hansen, from the Oval Office while they were still in lunar orbit, he described their achievement as proof that "America doesn't just compete, we dominate." The phrase was doing diplomatic work well beyond its face value. The audience it was really addressed to was in Beijing.

The Artemis II mission itself was, technically, a test flight. No moon landing, no flag, no footprints. The Orion spacecraft looped around the far side of the Moon, checked its life-support systems against the unforgiving radiation environment of deep space, and came home. In the punch-counterpunch style of the 1960s, China's response could be coming within months, the China National Space Administration is scheduled to launch Chang'e 7 in the second half of 2026, an uncrewed mission targeting the lunar south pole. The distance between Apollo and Artemis was fifty years of geopolitical dormancy. The distance between Artemis II's splashdown and the next competitive move is measured in calendar quarters.

This is what the return of Big Science actually looks like in 2026: not leisurely exploration driven by human curiosity, but a sprint for physical presence on terrain that both Washington and Beijing have identified as strategically decisive. The 1960s space race was about prestige and ideology. This one is about property.

The terrain in dispute

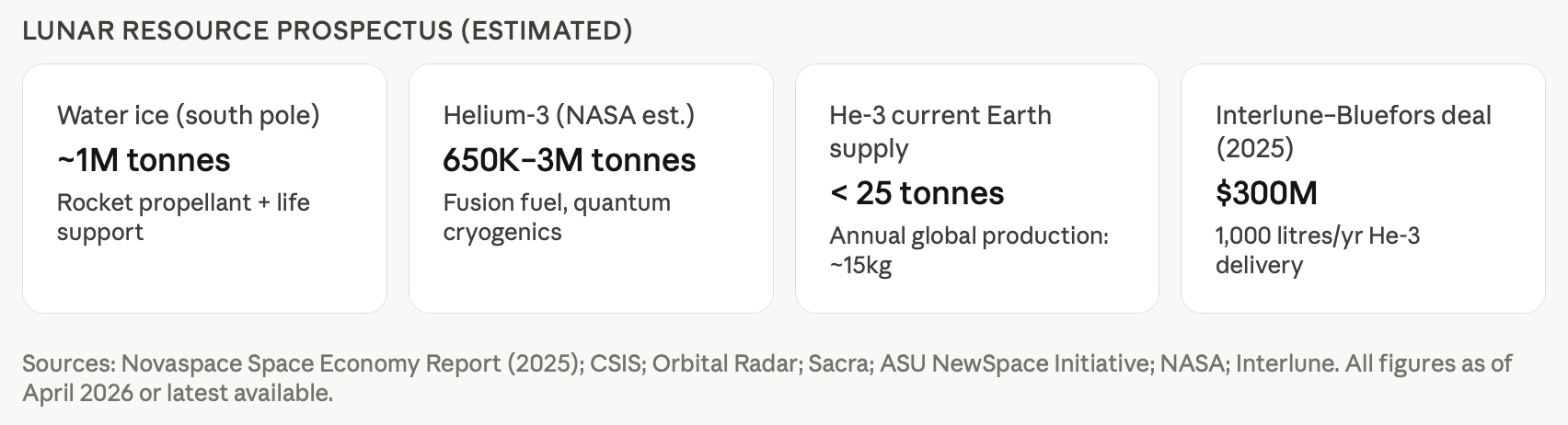

The Moon's south polar region is not a poetic destination. It is, from a resource standpoint, the most valuable real estate in the inner solar system. Permanently shadowed craters near the south pole are believed to hold water ice, chemically distinct from Earth ice, which could theoretically be converted into rocket propellant and oxygen for breathing, effectively turning the Moon into a self-sustaining refueling station for deep-space exploration.

Water ice is only the beginning. Helium-3, an isotope extraordinarily rare on Earth but scattered across the lunar surface by solar winds over billions of years, has attracted significant attention as a potential fuel for clean fusion reactors, as a cryogenic coolant for quantum computing hardware, and as a medium for advanced medical imaging. NASA estimates total lunar helium-3 reserves at somewhere between 650,000 and three million tonnes. Total current terrestrial supply is under 25 tonnes. Theoretically, 25 to 30 tonnes of lunar helium-3 could fuel nuclear fusion power plants providing all the energy the United States consumes in a year.

These numbers invite skepticism, and they deserve it. The concentration of helium-3 in lunar regolith is extremely low, to extract commercially meaningful quantities, miners may have to process enough lunar soil to fill a backyard swimming pool just to obtain a few liters. Interlune, the Seattle-based startup founded by former Blue Origin president Rob Meyerson, has built a prototype excavator designed to process 100 metric tonnes of lunar soil per hour, but that prototype has not yet left Earth, let alone operated in the vacuum and extreme temperature swings of the lunar surface. The engineering gap between laboratory demonstration and operational lunar mining remains vast.

Yet the business arrangements are already being written. In September 2025, Helsinki-based cryogenics firm Bluefors signed an agreement with Interlune to purchase up to 1,000 liters of lunar helium-3 annually, in a deal valued at roughly $300 million. In mid-2025, the U.S. Department of Energy made what was described as the first government purchase of an extraterrestrial resource, a procurement of three liters of lunar helium-3, intended to seed early supply chains and signal strategic interest. Private buyers including Maybell Quantum and Microsoft have also begun positioning for supply arrangements. The market is pricing future extraction before a single kilogram has been lifted off the lunar surface.

The analogy here is not the California Gold Rush. It is more precisely the early oil concession agreements of the 1920s, commercial contracts for resources whose full scale was unproven, written in advance of the infrastructure needed to extract them, animated less by current economics than by the strategic logic of first-mover advantage. Observers compare the modern rare-earth story, where concentrated production in China now shapes entire global supply chains and confers substantial geopolitical influence, as the reason governments are moving now, the prospect of a similar asymmetry on the Moon is the primary driver of urgency.

The two operating systems

In direct response to the U.S.-led Artemis program, China and Russia have partnered on the International Lunar Research Station (ILRS), envisioned as a comprehensive scientific facility on the lunar surface near the south pole, developed in three phases through 2045. Its partners include Pakistan, Egypt, South Africa, and Venezuela, a distinct non-Western coalition in space exploration.

The architectural contrast between the two programs is instructive. The United States is running its lunar ambitions through a public-private model that has no real historical precedent at this scale. While NASA provides the overarching vision, funding, and foundational government hardware, it has outsourced mission-critical component development to commercial partners, a strategy that introduces significant vulnerability, as Artemis timelines are now linked to commercial partner performance. SpaceX's Starship, which serves as the Human Landing System for Artemis III, has completed 11 integrated test flights through late 2025, and NASA's Artemis III crewed landing has already slipped to 2028 partly due to Starship development challenges.

China is operating a more traditional model, patient, state-directed, and funded at a level that makes direct cost comparisons difficult. Over the last decade, China has spent over $104 billion on civil, military, and commercial space efforts. That is roughly one-fifth of estimated U.S. spending over the same period, but the trajectory line is steep. Chinese investment in its commercial space sector grew from $340 million in 2015 to $3.81 billion in 2025, a more than tenfold increase in a decade. In 2025, China conducted what many observers believe was the world's first satellite refuelling operation in geosynchronous orbit and is ramping up toward a 300-satellite surveillance constellation in very low Earth orbit.

China has also inaugurated the International Deep Space Exploration Association (IDSEA), designed with a rotating council to mitigate fears of Chinese dominance by mimicking multilateral U.N. structures, and framing planetary defense and access to the space economy as a "shared mission for all humanity." It is sophisticated soft-power architecture: an institutional framework designed to accumulate coalition partners by offering something the Artemis Accords do not, non-Western governance weight.

If China lands astronauts on the Moon first, as former NASA astronaut and space policy analyst Terry Jones has noted, Beijing would use the achievement to tout its political system's effectiveness and its military and aviation technology exports. The geopolitical cost to Washington of that outcome would be substantial, and it is this calculation, not pure scientific ambition, that explains why NASA Administrator Jared Isaacman announced in late March a dramatic restructuring of the agency's priorities, pausing work on Lunar Gateway (the planned multinational space station) to concentrate resources on the moon base itself. "The clock is running in this great-power competition," Isaacman said, "and success or failure will be measured in months, not years."

The capital event of the century

Against this backdrop, SpaceX's IPO filing represents more than an investment opportunity. It is a structural transformation of the space economy itself.

SpaceX confidentially filed for an IPO on April 1, 2026, targeting a valuation above $2 trillion, with 21 banks lined up including Morgan Stanley, Goldman Sachs, and JPMorgan competing for lead roles. The filing aims partly to raise capital to fund up to one million AI data-center satellites. To put that valuation in context: it would make SpaceX roughly twice the size of Saudi Aramco at the time of its 2019 IPO, the previous record-holder for largest public offering.

SpaceX is projected to achieve revenue of approximately $15–16 billion in 2025, with EBITDA of around $8 billion. Bloomberg analysts expect combined revenue from the launch business and Starlink to approach $20 billion by 2026. Starlink has now surpassed 10 million global subscribers, generating estimated revenue of $10.6 billion in 2025 with profit margins approaching 54%. That is not speculative astrophysics. That is a telecommunications business that happens to operate from orbit.

The IPO is, however, a genuinely complicated investment proposition. SpaceX is simultaneously the backbone of NASA's lunar program, a satellite broadband operator competing with terrestrial carriers, an AI data-center infrastructure company in embryonic form, and Elon Musk's personal geopolitical instrument. Risks include valuation multiples above 125 times revenue, unachieved technological breakthroughs, particularly around Starship's full orbital capability and mounting questions about the synergy between the rocket and AI businesses. As one veteran investor noted, the SpaceX IPO is essentially a high-stakes bet on whether humanity can genuinely enter the space age on a commercially sustainable timeline.

The global space economy was valued at $626 billion in 2025, with the commercial sector accounting for approximately 78% of the total. Analysts converge on the space economy crossing $1 trillion between 2032 and 2034, driven by satellite broadband, defense modernization, and the emergence of in-space manufacturing and servicing. SpaceX, were it valued at $2 trillion at IPO, would be worth more than three times the entire current annual commercial space economy.

The shakeout this triggers in the rest of the industry is already visible. Launch competitors like Rocket Lab, United Launch Alliance, and Europe's Ariane 6 do not compete with SpaceX on price, they exist primarily to provide sovereign industrial redundancy. In China, 2026 has been declared the "Year of Commercial Space," with breakthroughs in reusable rocket technology expected to push the industry from a policy incubation phase to large-scale implementation, and Landspace becoming China's first commercial space stock on the A-shares Science and Technology Innovation Board. This is not China catching up. This is China building its own operating system.

The legal vacuum at 238,855 miles

The governance framework for all of this activity is, charitably described, incomplete. The 1967 Outer Space Treaty establishes that no nation can own a celestial body. It says nothing definitive about mining one. The 1979 Moon Agreement, which would have classified lunar resources as the "common heritage of mankind," was ratified by 18 countries, none of whom have actually landed on the Moon.

The Artemis Accords, signed now by 61 nations, affirm that resource extraction in outer space is lawful under certain conditions. China and Russia, which are planning a permanent base together at the moon's south pole, are not signatories. The result is two competing international legal frameworks for the same physical terrain, with no enforcement mechanism for either. Early permanent presence may, in practice, confer operational control regardless of what the treaties say which is precisely why the race for first boots on the lunar south pole has taken on the character it has.

Geopolitics are a further uncertainty: whoever establishes a stronger presence could take the lead in setting rules for lunar operations, including mining. If the ILRS and Artemis blocs operate under conflicting interpretations of safety and property, the Moon could face incompatible legal frameworks and accidental interference could, in a worst-case scenario, spiral into terrestrial geopolitical conflict.

There is also the question of what the Moon is for. Scientists note that mining operations raise questions not only about resource rights but about the preservation of scientifically irreplaceable terrain, including the permanently shadowed craters whose very untouched state makes them unique repositories of solar system history. Andrea Harrington, co-director of McGill University's Institute of Air and Space Law, has been explicit: "If you try to carry out dominance to mean exclusion of others, that is absolutely unlawful under international law." The Outer Space Treaty does not permit sovereignty. The gap between "permanent presence" and "effective control" is where the most consequential legal battles of the next decade will be fought.

Within this context, a bipartisan group of U.S. senators has proposed the Space RACE Act, which would create a National Institute for Space Research a federally controlled but independently operated entity designed to coordinate U.S. research leadership as the International Space Station retires in 2030. The timing is pointed: NASA is simultaneously facing a proposed 24% budget cut in fiscal 2026 under the White House's proposal, with the science program facing a 47% reduction. The administration is betting that commercial sector dynamism can compensate for reduced government science funding. History offers mixed evidence for that hypothesis.

The skeptic's assessment

It is worth pausing on what we actually know, as opposed to what is being projected.

Humanity has not landed on the Moon in 54 years. The hardware required to do so under Artemis specifically Starship's performance as a lunar lander, has not yet demonstrated full orbital capability. China has never conducted a crewed spaceflight beyond low Earth orbit. Lunar helium-3 extraction remains, at present, a prototype excavator and a series of forward purchase agreements. The resource estimates for water ice and helium-3 are based on orbital spectroscopy and Apollo-era sample analysis, not the direct subsurface characterization that commercial extraction would actually require.

The space economy's $626 billion current valuation is real, but it is overwhelmingly satellite telecommunications, GPS, Earth observation services, and existing government programs. The genuinely new layer, cislunar infrastructure, in-space manufacturing, resource extraction remains speculative at commercially meaningful scale.

None of this invalidates the strategic logic. The Apollo program produced integrated circuits, water filtration systems, scratch-resistant lenses, and memory foam. The GPS constellation underpins an estimated $1.4 trillion in annual U.S. economic activity. Big Science has a documented record of spinning off economic value that vastly exceeds the cost of the original program. The question is not whether a serious lunar presence would generate enormous downstream value. It almost certainly would. The question is whether the timelines being projected by both governments and investors are grounded in engineering reality, or in the kind of optimistic extrapolation that has historically characterized the early innings of every space boom.

As Jonathan Roll, a program manager at Arizona State University's Space Technology and Science Initiative, has observed: "The stakes are higher than those of the 1960s race between the U.S. and Soviet Union." In the 1960s, the prize was symbolic. The technology generated was almost incidental. This time, the technology is the prize, and the nations and companies that establish technical standards, supply chain dominance, and physical infrastructure in cislunar space will be in a position to extract value from it for decades.

The power loom did not eliminate the textile industry. It reorganized it entirely concentrating capital, displacing labor, and creating new categories of wealth at a speed that existing institutions could not absorb. The current convergence of geopolitical competition, commercial capital, and declining launch costs may be doing something similar to the relationship between nations and space. The terrain is no longer primarily a destination. It is becoming an economic zone. What the rules of that zone will be, who writes them, and who enforces them is the defining geopolitical question of the next quarter century.

That question will not be settled in congressional hearings, bilateral treaties, or U.N. resolutions. It will be settled by who lands first, who stays longest, and who builds the infrastructure that makes departure inconvenient.

Corrections and tips: readers with specific technical knowledge of the Starship Human Landing System development schedule, ILRS construction timelines, or lunar helium-3 concentration data are encouraged to write.