WHAT'S NEWS

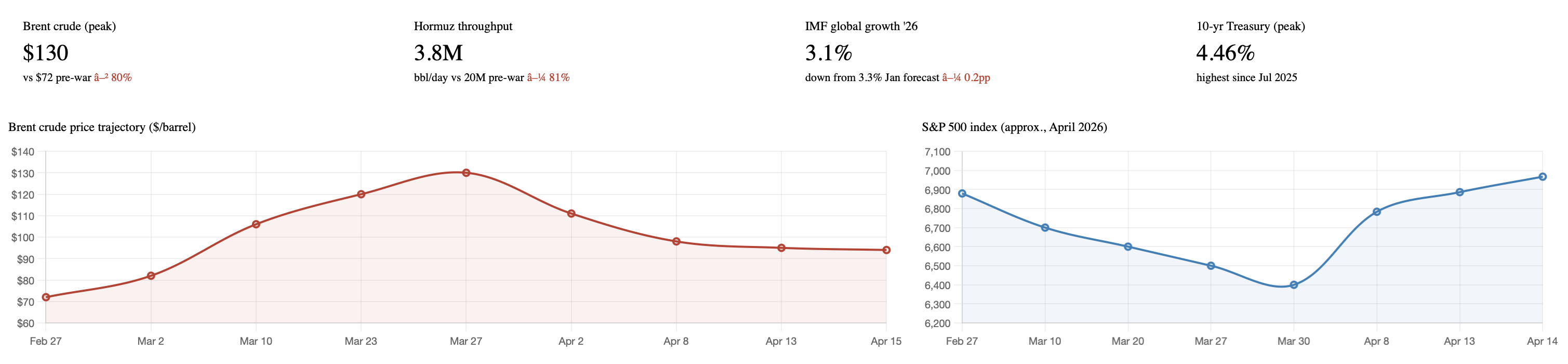

The closure of the Strait of Hormuz in early March 2026 produced what the International Energy Agency has characterised as the largest supply disruption in the history of the global oil market, cutting Hormuz throughput from 20 million barrels per day to just 3.8 million by early April.

The IMF downgraded its 2026 global growth forecast to 3.1% from 3.3%, while marking up its inflation projection to 4.4% - with a "severe scenario" in which energy shocks persist potentially dragging global growth to 2% in both 2026 and 2027.

The S&P 500 erased all war-driven losses on April 13, climbing back above 6,878 - the level it traded at just before hostilities began on February 28 buoyed by ceasefire optimism and a strong opening to earnings season.

Fifty-three years after Arab members of OPEC weaponised oil supply and reshaped the postwar economic order, the Strait of Hormuz has done it again. This time, the chokepoint's closing was not a political embargo but a kinetic one: Iran shutting the 21-mile-wide passage with mines, anti-ship missiles, and the wreckage of tankers that gambled wrong.

The result is the same operatic disruption that haunts every energy economist's nightmare scenario only with the volume turned up. The 1973 oil embargo removed roughly 7% of global supply. The 2026 Iran war fuel crisis has disrupted approximately 20% of global oil supplies and significant LNG volumes simultaneously, a shock magnitude that makes the prior crises look like rehearsals.

The immediate arithmetic is brutal. North Sea Dated crude briefly hit $130 per barrel, while physical cargoes for immediate delivery traded $20 to $30 above futures benchmarks a spread that signals not just scarcity but outright desperation among refiners unable to source spot supply. In Singapore, the financial hub through which much of Asia's energy trading flows, middle distillates reached all-time highs above $290 per barrel, reflecting the extremity of refiners' positions.

The stock market's initial response followed the classic war playbook panic, then reassessment. The Dow Jones Industrial Average, the Nasdaq Composite, and the S&P 500 all slid toward correction territory following the initial U.S.-Israeli strikes on Iran. At the March 30 trough, the S&P 500 had shed approximately 7.5% from pre-war levels painful but orderly, the kind of move that speaks to institutional discipline rather than retail rout. The CBOE Volatility Index, Wall Street's fear gauge, peaked at an intraday high of 31.65 on March 27, a level that implies meaningful tail-risk pricing but stops well short of the pandemic-era panic readings above 80.

Then came the ceasefire bounce. When President Donald Trump announced a two-week suspension of strikes on Iran on April 7, the Dow ripped 1,325 points higher its best single-day performance since April 2025 while WTI crude tumbled more than 16%, its largest daily drop since April 2020. Markets, it turned out, were not pricing a protracted war. They were pricing uncertainty about its duration. Remove the uncertainty, even temporarily and assets reprice violently in the other direction.

The Machinery Behind the Shock

To understand why this crisis bites so differently than its predecessors, you have to understand what actually moves through the Strait of Hormuz. It is not merely oil. It is the integrated supply chain of the modern global economy: crude oil, refined petroleum, liquefied natural gas, diesel, jet fuel, sulfur for fertilisers, and critically for semiconductor and photovoltaic manufacturing tungsten.

Qatar, Kuwait, and Iran together produce and export roughly 45% of globally traded sulfur, an essential feedstock for fertiliser and pesticide industries. Tungsten critical for armor-piercing ammunition but equally essential for semiconductors, photovoltaics, aerospace, and high-precision manufacturing saw its price surge more than 50% in March 2026, more than tripling since December 2025, as China simultaneously restricted exports of a mineral it supplies in 80% of global volume.

This is the compound shock that distinguishes 2026 from 1973. In the 1970s, oil was primarily an energy input. Today, oil and its co-products are woven through virtually every industrial process, and a single chokepoint disruption cascades through fertilisers, food costs, petrochemicals, shipping, and military supply chains simultaneously.

Iran's retaliatory attacks on U.S. bases in Qatar, the UAE, and Bahrain injected further uncertainty into global markets, and QatarEnergy suspended LNG production after an Iranian drone strike on March 2 removing Qatar's 20% share of global LNG supply from the market in a single day. For Europe, still operating with gas storage levels estimated at just 30% capacity following a harsh 2025–2026 winter, Dutch TTF gas benchmarks nearly doubled to over €60 per megawatt-hour by mid-March.

The European dimension is acutely uncomfortable for policymakers who believed the post-Ukraine energy restructuring had made the continent more resilient. It hadn't it had merely substituted Russian pipeline gas for Qatari LNG, trading one vulnerability for another.

The Fed's Impossible Position

Monetary policymakers are caught in a configuration that economic theory handles poorly: a supply-side inflation shock arriving into an economy where price levels are already elevated and rate cycles are mid-course.

The 10-year Treasury yield jumped to 4.46% on March 27, its highest level since July 2025 a move that reflected not just war-risk premium but the market's expectation that the Fed would face renewed pressure to hold rates higher for longer. The IMF's revised scenario models make the trade-off explicit: in its "severe scenario," in which energy shocks persist into 2027 and central banks are forced to raise interest rates to combat inflation, global growth could drop to 2% for two consecutive years.

The U.S. economy's particular vulnerability stems from its already-strained pre-war position. The expansion of military conflicts in the Middle East has posed a new shock to a U.S. economy already struggling with tariffs, persistent inflation, and declining employment. The IMF's revised U.S. growth forecast of 2.3% for 2026 looks achievable only under the assumption that the ceasefire holds a bet the bond market is evidently unwilling to make at anything approaching face value.

Despite this, corporate earnings have so far surprised to the upside. Analysts expect S&P 500 earnings to grow roughly 13% in the first quarter of 2026, which would mark the sixth straight quarter of double-digit gains a data point that partially explains why equity markets have recovered so sharply. Put simply: the war has damaged macro confidence more than it has damaged corporate cash flows, at least so far. That divergence may not persist if energy prices remain elevated into the second half of the year.

Asia's Acute Exposure

If Europe is uncomfortable, Asia is in genuine emergency mode. Approximately 84% of the crude oil and 83% of the LNG that passed through the Strait of Hormuz in 2024 was bound for Asia, with China, India, Japan, and South Korea accounting for nearly 70% of those oil shipments.

The Philippines moved first. On March 24, 2026, President Bongbong Marcos declared a state of national energy emergency, the first country in the world to do so following the outbreak of the war given that the Philippines imports 98% of its oil from the Middle East. Government offices shifted to a four-day working week to conserve fuel.

The broader lesson for Asian economies is structural: the avenues that allowed Europe to navigate the post-Ukraine gas shock rapid LNG diversification, aggressive demand management, intensive storage accumulation are largely unavailable in Southeast Asia. Most of the region lacks the infrastructure for rapid supply substitution, the storage capacity for meaningful reserves, or the financial depth to absorb prolonged price spikes without social consequences.

China, notably, is better positioned partly by design, partly by the geopolitical foresight of stockpiling oil before the conflict escalated. But even Beijing is not insulated. Global observed oil inventories fell by 85 million barrels in March, though inventories within the Middle East and China actually rose, essentially trapped behind the blockade or held in floating storage, while stocks in importing Asian countries dropped 31 million barrels.

The Insider Trade Question

No crisis of this magnitude passes without market integrity questions, and this one is no different. A Financial Times investigation found that $580 million in bets on falling oil prices had been placed with the stock market via futures positions just 15 minutes before Donald Trump published his statement on March 23 postponing attacks on Iran for talks causing oil prices to fall temporarily triggering speculation about insider trading and calls for further investigation.

The SEC has not yet commented publicly on the investigation. The timing is striking enough to warrant serious scrutiny regardless of where the inquiry leads. Energy futures markets are among the most heavily traded in the world; even a brief directional edge on a presidential announcement of this magnitude is worth hundreds of millions of dollars. Whether or not the trades reflect something improper, the episode underscores a broader problem: geopolitical markets reward proximity to decision-makers, a structural advantage that retail and institutional investors without Washington access simply cannot replicate.

The Acceleration No One Expected

The most consequential long-run consequence of this shock may be the one least reflected in current asset prices: the structural acceleration of the energy transition.

IEA Executive Director Fatih Birol said countries were likely to pivot to renewables as a way to mitigate geopolitical risks describing the energy transition as moving "very strongly" before the Iran war began, and noting that the fallout from the energy shock means countries will likely direct even more investment toward clean energy.

The framing has shifted. Clean energy is no longer being sold primarily as a climate solution. The IEA's Fatih Birol told reporters that the main driver will not be climate change the main driver will be energy security, with renewables' appeal now rooted in the fact that they are homegrown, domestic energy sources.

The economics already support the pivot independent of geopolitics. Solar PV now produces power at 4.4 cents per kilowatt-hour and onshore wind at 3.3 cents, compared to roughly 10 cents for fossil-fuel alternatives. Countries added a record 700 gigawatts of new renewable capacity in 2025, and the International Renewable Energy Agency reports that 92% of the world's installed renewable capacity is now cheaper than fossil-fuel alternatives.

Renewables accounted for 85.6% of all new energy capacity installed worldwide in 2025, with renewables now comprising a record 49.4% of the world's total energy capacity, up from 46.3% in 2024.

The historical analogy is instructive here. The 1973 oil embargo ultimately produced the lithium-ion battery not immediately, not directly, but through a chain of research investment triggered by the recognition that dependence on a foreign chokepoint was an existential economic risk. The war on Iran may prove to be the 1973 moment for grid-scale storage, for offshore wind, and for nuclear small modular reactors. The Bulletin of the Atomic Scientists notes that the conflict will likely hasten adoption of nuclear power programs globally even in conflict-prone areas driven by the need for firm, non-intermittent power that complements renewable penetration.

Investors are already trying to position for this. During the sell-off from February 27 through March 30, energy was the only sector in the green, rising 11% while tech fell 8%. Since the March 30 low, that script reversed sharply: tech jumped 13% while energy fell 8% suggesting the market is not simply pricing a prolonged war economy, but reaching back toward the pre-war bull-market playbook of AI-driven productivity growth.

A word of caution on the transition narrative, however, is warranted. Renewables are not immune to geopolitical disruption their supply chains also run through a dangerous world. Rare earths, critical minerals, and other raw materials are often mined and processed abroad, and shipped through the very maritime lanes carrying oil and LNG. Swapping one strategic dependency for another is not the same as achieving energy security. The geography changes; the vulnerability does not fully disappear.

The Bottom Line for Investors

The ceasefire announced April 7-8 removed the acute tail risk of all-out sustained conflict, and markets have responded rationally S&P 500 effectively flat from pre-war levels as of April 14, VIX retreating from 31.65 toward 20, and oil futures sliding from $130 toward the mid-$90s. Even if the truce holds and military activity winds down, the restart of energy production and exports will take time. Damage to LNG facilities, refining capacity, and production infrastructure may take months to come back online, and engineering constraints mean restarts are often drawn out, with equipment integrity risks if operations resume too quickly.

Morgan Stanley's Mike Wilson declared that "the lows are in" and pointed to rotation back into pro-cyclical market segments as evidence that things are likely to "resolve constructively in the second half of this year." Ed Yardeni maintains a year-end S&P 500 target of 7,700 and has written that financial markets "may be learning to live with the war in the Middle East, as they have with the war between Ukraine and Russia." Those are constructive readings though, it should be noted, they assume no re-escalation, a working ceasefire, and a Strait that progressively reopens.

The base case for sophisticated investors is probably this: energy prices stay elevated for longer than futures currently price, the inflation impulse keeps monetary policy tighter than pre-war expectations, and economic growth decelerates modestly but does not collapse. Against that backdrop, the strategic winners are: integrated energy producers with diversified assets outside the Gulf, renewable energy companies with defensible supply chains, AI and software companies whose cash flows are relatively insulated from energy costs, and financial institutions capable of pricing and hedging geopolitical risk premiums.

The losers are clear enough: highly leveraged cyclicals, Asian import-dependent economies without natural gas alternatives, and any business model whose input cost structure is inextricably tied to Middle Eastern energy airlines, shipping, petrochemicals, and fertiliser producers among them.

What is harder to price and what the market has not yet fully grappled with, is the regime shift. If this conflict establishes that a single actor can close 20% of global oil supply with missiles and mines, the risk premium embedded in all energy assets must structurally reprice upward. That is not a 2026 story. It is a decade-long story, and the first chapter has just been written.

CORRECTIONS & AMPLIFICATIONS

This article draws on data available as of market close April 14, 2026. Oil price figures cited reflect Brent crude futures and physical spot-market prices as reported by the IEA monthly report released April 14, 2026. IMF growth and inflation forecasts are drawn from the April 14, 2026 World Economic Outlook. S&P 500 and DJIA closing figures are sourced from CNBC and Motley Fool market data reports. Any material inaccuracies should be reported to the editorial desk.