For much of the past three years, consumers have been told the same story. Supply chains will heal. Inventories will recover. Competition will return. Prices, inevitably, will fall back to something resembling normal.

That normal is not coming back.

New car prices have stabilised in some segments, incentives have cautiously reappeared, and production volumes have improved. Yet the fundamental economics of the automotive industry have shifted in ways that make a broad, lasting price correction unlikely. What we are seeing now is not a temporary distortion. It is a structural reset.

To understand why, you have to look past dealership markups and interest rates and examine how the car business itself has changed.

The Myth of the Supply Chain Rebound

The original justification for rising prices was simple. Pandemic disruptions, semiconductor shortages, and logistics breakdowns constrained supply while demand rebounded faster than expected. That explanation was valid, up to a point.

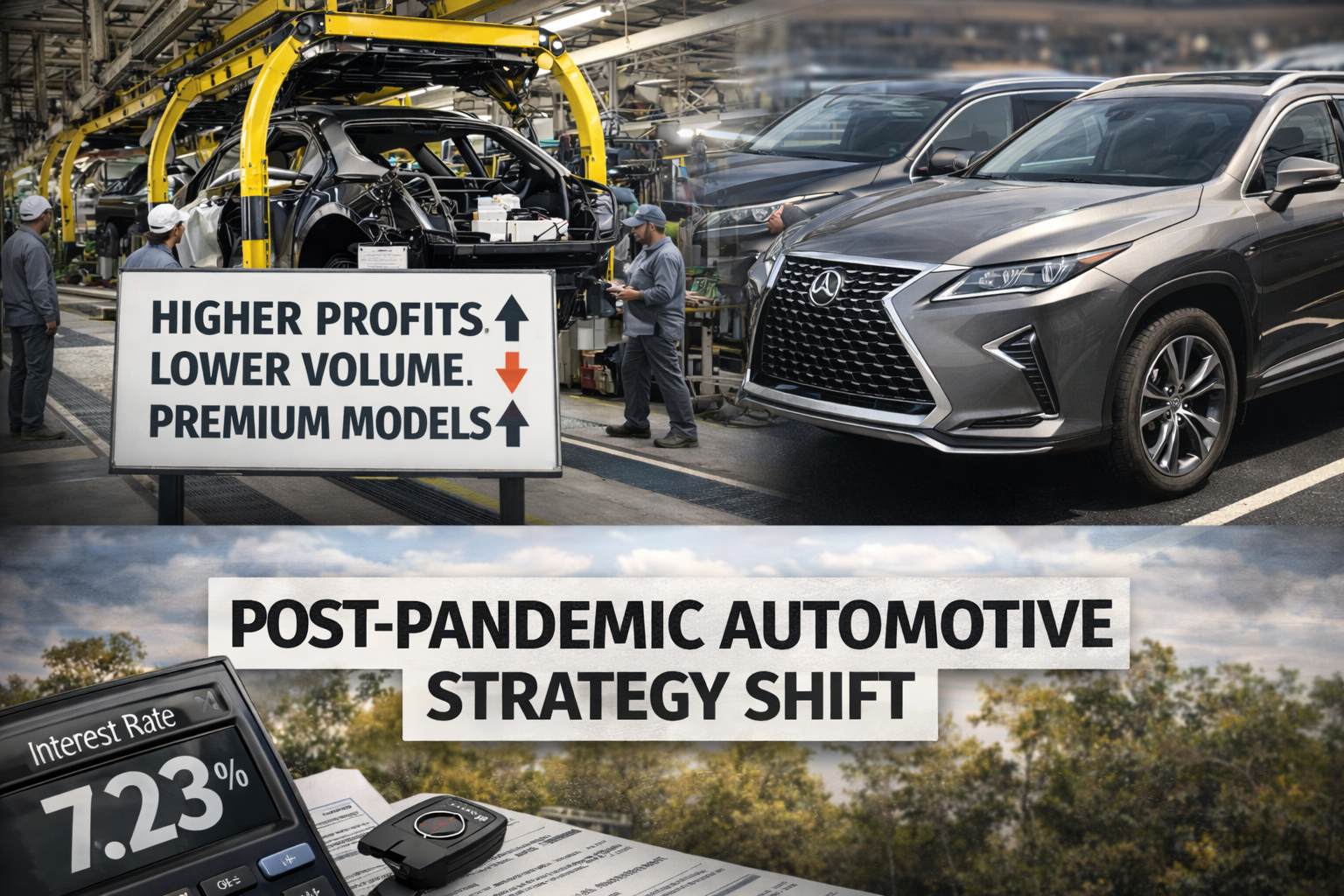

What has become clear since is that manufacturers learned something during the shortage years. They discovered that selling fewer cars at higher margins was not only possible, but preferable.

Before 2020, much of the industry operated on volume-driven logic. Plants were run near capacity. Incentives were used aggressively to clear inventory. Profitability depended on scale, not restraint. When supply collapsed, automakers were forced to prioritise which vehicles to build. Predictably, they chose higher-margin trims, better-equipped models, and premium variants.

The result was a revelation. Revenue held up, and in many cases improved, despite lower unit sales. That lesson has not been forgotten.

A Permanent Shift in Manufacturer Strategy

Major manufacturers, including Toyota and Ford, have been unusually candid about their post-pandemic approach. Inventory discipline is no longer framed as a crisis response. It is now positioned as good business.

Lower dealer stock reduces the need for incentives. It shortens sales cycles. It gives manufacturers greater control over pricing and mix. From their perspective, flooding lots with excess vehicles was never efficient. It was simply tradition.

There is little incentive to return to that model.

Even as production capacity recovers, automakers are pacing output more deliberately. This is not an inability to build cars. It is a choice about how many to release into the market at any given time.

The Cost Floor Has Moved Up

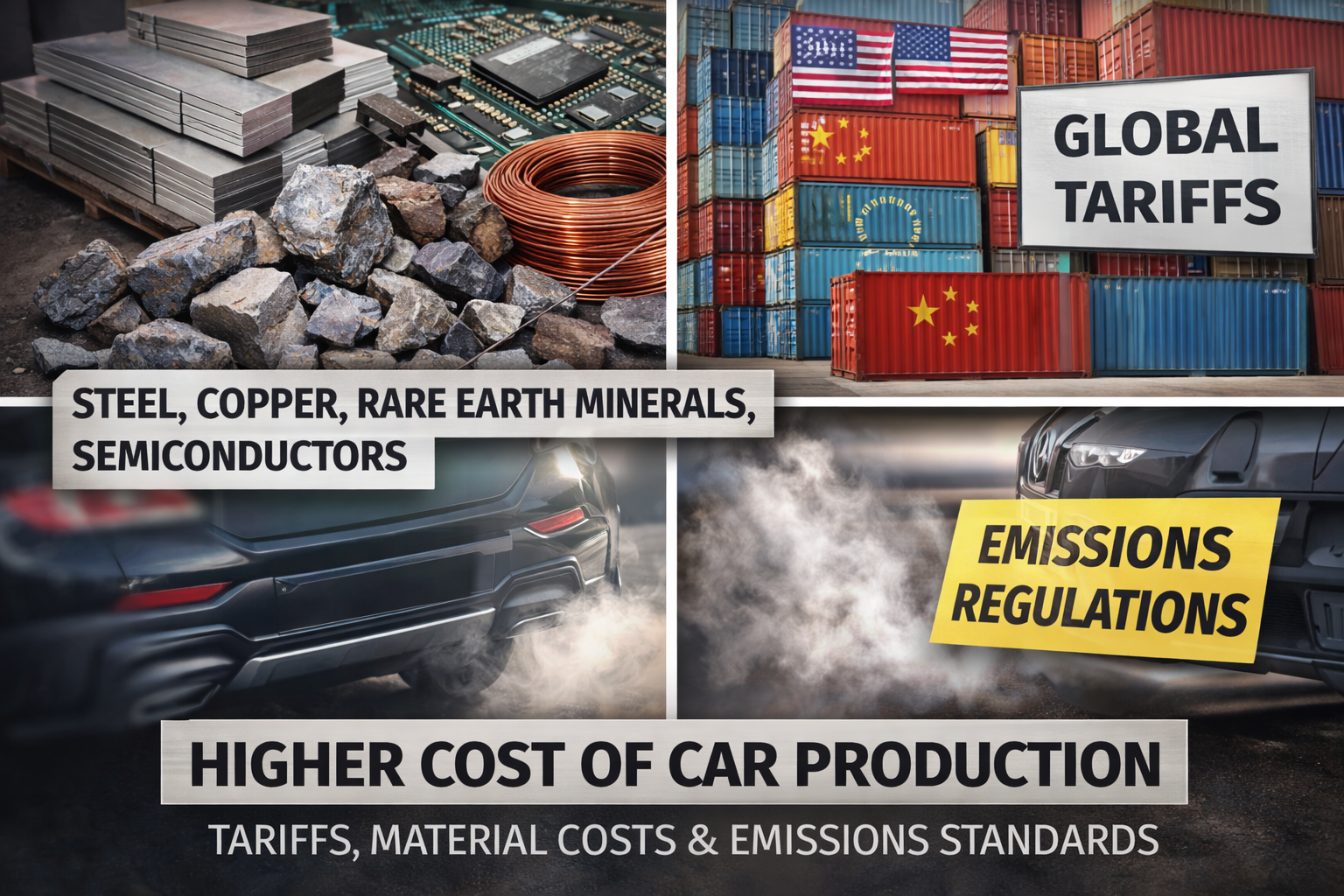

Even if manufacturers wanted to push prices down, they would face a hard reality. The cost of building a modern car is significantly higher than it was five years ago.

Materials matter. Steel, aluminium, plastics, and rare earth elements have all experienced volatility. Labour costs have risen, not only in assembly plants but throughout the supplier network. Logistics remain more expensive and more complex than in the pre-pandemic era.

Then there is technology. Advanced driver assistance systems, larger infotainment displays, stricter emissions controls, and increased crash safety requirements are no longer optional. They are baked into the baseline vehicle. Entry-level cars now carry equipment that would have been considered premium a decade ago.

That equipment costs money, and it has permanently raised the industry’s cost floor.

Regulation Without Price Relief

Regulatory pressure has also played a role. Emissions standards continue to tighten in major markets, forcing manufacturers to invest heavily in compliance technologies. Electrification, whether through hybrids or full battery-electric vehicles, requires enormous capital expenditure.

These costs are not absorbed quietly. They are amortised across vehicle pricing.

Crucially, regulation has not reduced consumer expectations. Buyers still expect longer warranties, higher reliability, and greater performance. Manufacturers are required to deliver more while spending more. There is no hidden margin waiting to be given back.

Financing Has Changed the Conversation

Much of the shock around modern car prices is psychological. Monthly payments, not sticker prices, have long been the real metric for most buyers. For years, low interest rates masked rising vehicle costs. Longer loan terms smoothed the numbers. Leasing absorbed depreciation risk.

As interest rates rose, that illusion collapsed.

Higher borrowing costs have exposed how expensive cars already were. But this does not mean manufacturers will lower prices to compensate. Financing conditions are largely outside their control, influenced by central banks such as the Federal Reserve and global monetary policy.

Automakers have historically responded to tight credit with targeted incentives, not systemic price reductions. That pattern is repeating now.

Used Cars Are No Longer a Release Valve

In the past, the used market acted as a pressure release. When new cars became expensive, buyers flowed downmarket. Supply increased. Prices softened.

That mechanism has broken.

Fewer new cars sold during the shortage years means fewer used cars entering the market now. Lease returns are down. Fleet turnover slowed. Vehicles are being kept longer. The result is a used market that remains structurally tight, especially for desirable late-model vehicles.

Without abundant used supply, there is no downward pull on new car pricing.

Consumer Adaptation, Not Resistance

Perhaps the most uncomfortable truth is that consumers have adapted. Buyers are stretching loan terms, accepting higher payments, and recalibrating expectations. Demand has softened at the margins, but it has not collapsed.

As long as cars continue to sell at current prices, manufacturers have no incentive to reverse course. Market behaviour, not public frustration, sets pricing reality.

The New Normal

Car prices are not high because the system is broken. They are high because the system is working exactly as its major players now prefer.

Lower volumes, higher margins, controlled supply, and technology-rich products define the post-pandemic automotive economy. Absent a severe recession or regulatory intervention, there is no natural force pushing prices meaningfully downward.

What consumers are experiencing is not a temporary spike. It is a redefinition of value, cost, and expectation.

The era of cheap new cars was built on excess, incentives, and volume at all costs. That era is over.